VAM! Volatility-Adjusted Multiplier

AiM.VAM is an indicator study for TradeStation. The values are published in the ETF tab of the members-only weekly workbook.

How much cash should I hold in this volatile market?

The Volatility-Adjusted Multiplier (VAM) makes it easy for investors to manage their portfolio risk by adjusting the cash holdings based on market volatility. VAM is a number that is used to dynamically manage risk by decreasing exposure to more volatile assets. It can also be applied to potentially increase allocation to less volatile ones, all while aiming to maintain a consistent level of portfolio risk.

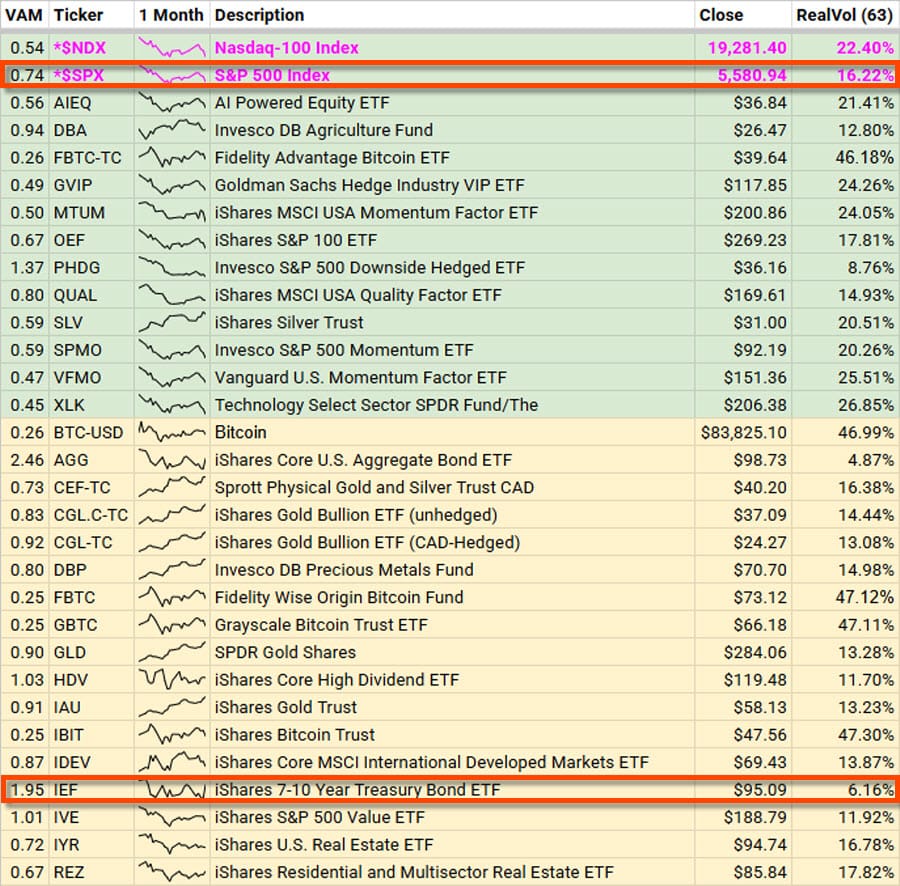

Let's apply VAM to the classic 60% stock and 40% bond allocation. For simplicity sake, let's assume the investor owns the S&P 500 Index using the SPDR® S&P 500® ETF Trust (SPY) or the Vanguard S&P 500 ETF (VOO), and owns 10-year Treasuries using iShares 7-10 Year Treasury Bond ETF (IEF) or the Vanguard Intermediate-Term Treasury ETF (VGIT).

Let's target a volatility of 12% and calculate the VAM:

Now apply VAM to the allocation to SPY or VOO:

The resulting volatility-targeted allocation would be:

We can see that VAM is part of a simple, yet sophisticated rule of thumb that provides a rough calculation of how much cash to hold for an existing portfolio. Historical volatility data is available at AlphaQuery.com.

Risk Parity

What about the 40% allocation to bonds? The 3-month realized volatility is only 6.16%. Using the same calculation:

Now apply VAM to the allocation to IEF or VGIT:

The resulting volatility-targeted allocation would be:

Any allocation greater than 100 percent requires the use of leverage or margin, or using futures or derivatives. We highly recommend do-it-yourself investors to avoid leverage, but those interested should read the case study on Ray Dalio's "All Weather" approach below because the concept of risk-parity is based on the idea that allocation to individual asset classes can be adjusted to target the volatility of the portfolio as a whole.

What is Volatility?

In simple terms, volatility refers to the degree of price fluctuations in stocks or other investments. When the market is volatile, prices are swinging up and down more dramatically than usual. Professionals typically measure volatility using a statistical tool called standard deviation, which quantifies how much returns deviate from their average over a specific period. Higher volatility means more unpredictable and potentially extreme price movements, while lower volatility suggests more stable and predictable price behavior.

How to Harness Volatility

For investment professionals, volatility is more than just a measure of price swings – it's a crucial indicator of financial risk. Volatility measures can be used to assess how much potential loss (or gain) an investment might experience. This understanding has led to the development of various strategies to manage and even capitalize on volatility.

One popular approach is low volatility investing. This strategy focuses on stocks that have historically shown less price volatility than the overall market. The idea is that these stocks can provide more stable returns over time, potentially outperforming their more volatile counterparts on a risk-adjusted basis.

Another way professionals use volatility is through dynamic portfolio management. They may adjust their portfolio's exposure to different assets based on current or expected volatility levels. For instance, during periods of high volatility, they might reduce exposure to riskier assets and increase holdings in more stable investments.

Benefits of Understanding Volatility

For individual investors, understanding volatility can provide several benefits. First, it improves risk management. By recognizing how volatile your investments are, you can better assess potential losses and decide if you're comfortable with that level of risk.

Second, understanding volatility can enhance portfolio construction. For example, combining low volatility strategies with other investment approaches can improve overall portfolio performance. This diversification can help smooth out returns over time, potentially providing a less stressful investment experience.

Third, focusing on volatility can lead to better risk-adjusted returns. Historically, low volatility strategies have generated higher risk-adjusted returns than the broader market. This means they've provided better returns relative to the amount of risk taken, which is a key goal for many investors.

Practical Applications for Individual Investors

So how can you apply this knowledge to your own investing? Start by assessing your personal risk tolerance. How much volatility can you handle without panicking and making rash decisions? This self-awareness is crucial for successful long-term investing.

Next, consider diversification strategies. By spreading your investments across different asset classes and sectors, you can potentially reduce overall portfolio volatility. Remember, not all investments react the same way to market events.

You might also consider incorporating low volatility investments into your portfolio. Many exchange-traded funds (ETFs) and mutual funds focus on low volatility stocks, providing an easy way for individual investors to access this strategy.

Cash Holdings in Volatile Markets

Now, let's address the question of cash holdings during volatile markets. Holding cash provides stability and flexibility during market turbulence. It can act as a buffer against losses and give you the ability to invest when opportunities arise. However, holding too much cash has downsides too. It may lead to missed opportunities if the market rebounds, and over the long term, cash tends to lose purchasing power due to inflation.

The right amount of cash to hold depends on your individual circumstances, including your risk tolerance, investment goals, and near-term cash needs. Beyond that, consider investing in a diversified portfolio that aligns with your risk tolerance and goals.

Case Study: Bridgewater's "All Weather" Approach

To better understand how professionals manage volatility and construct portfolios, let's examine a real-world example: Bridgewater Associates' "All Weather" strategy. Developed in 1996, this approach aims to create a portfolio that can deliver consistent returns across various economic environments, targeting a 10% return with 10-12% risk.

The "All Weather" strategy is based on what Bridgewater calls Post-Modern Portfolio Theory (PMPT). Unlike traditional portfolio management, which often results in concentrating risk in equities, PMPT separates returns into three components: the risk-free return (typically cash), beta (returns from asset classes), and alpha (returns from active management). This separation allows for more precise control over portfolio risk and return.

A key innovation in the "All Weather" approach is how it handles different asset classes. Instead of accepting the risk and return characteristics of assets as they come, Bridgewater adjusts them. They leverage up low-risk assets and de-leverage high-risk assets so that the expected returns and risks of all assets in the portfolio are roughly equal. This technique allows for much greater diversification than traditional portfolios.

For example, bonds, which typically have lower returns and lower volatility than stocks, are leveraged to have similar risk and return profiles to equities. This makes bonds "competitive" with higher-returning asset classes in the portfolio. By doing this, Bridgewater can create a truly diversified portfolio that doesn't rely heavily on any single asset class for its returns.

Recently, Bridgewater has made this strategy more accessible to individual investors through the SPDR Bridgewater All Weather ETF (ALLW), which was launched on March 5, 2025. This ETF provides an opportunity to examine how the strategy has evolved since its inception and how it's been adapted for a broader investor base.

The core philosophy of the "All Weather" approach remains consistent. It still focuses on creating a portfolio that is resilient across different economic environments. The strategy continues to emphasize balancing the portfolio against growth and inflation as the primary economic drivers. This aligns with the original concept of structuring a portfolio that can perform well regardless of the economic climate.

The ETF invests in a diverse range of assets, including equities, fixed income securities, inflation-linked bonds, and commodities. This broad diversification across asset classes is in line with the original strategy's emphasis on true diversification. However, the ETF structure has led to some evolution in implementation.

One notable change is the extensive use of derivatives, including futures contracts, forwards, swaps, and total return swaps. While derivatives were likely used in the original strategy, their prominence in the ETF structure is more explicitly stated. This may reflect both the need for efficient implementation in an ETF format and evolving market dynamics.

The Use of Leverage

The use of leverage, a key component of the original strategy, continues in the ETF. The prospectus notes that the leverage can be "substantial". In the original strategy, Bridgewater typically employed about 2 times leverage, which was actually less than the average large company in the S&P 500. However, the ETF prospectus doesn't mention a specific leverage target in the main strategy section.

The ETF maintains the original strategy's volatility target, aiming for an annualized volatility level for the portfolio ranging between 10%-12%. This consistency in volatility targeting demonstrates the continued importance of risk management in the strategy.

An interesting evolution is the explicit mention of "environmental balance" as a key concept. While this idea was present in the original strategy, its formalization suggests a refinement of the approach over time. The strategy still focuses on balancing risk across different economic environments - particularly across scenarios of rising and falling growth and inflation.

Another notable change is the indication of more active management. While the core strategy remains systematic, the prospectus states that Bridgewater may vary allocations based on its assessment of market conditions and evolutions in its understanding. This suggests a blend of the original systematic approach with more dynamic adjustment based on market insights.

Interestingly, the prospectus explicitly states that Bridgewater does not vary weights based on tactical views of how particular investments will perform. This reinforces the strategic, long-term nature of the approach, which has been a hallmark of the strategy since its inception.

The "All Weather" strategy demonstrates how a deep understanding of volatility and risk can lead to innovative portfolio construction techniques. By leveraging lower-risk assets and de-leveraging higher-risk ones, it aims to achieve a more consistent return stream across different market conditions. This approach challenges the conventional wisdom that higher returns always require taking on more risk.

For individual investors, while directly replicating such a complex strategy may not be feasible, there are valuable lessons to be learned. The importance of true diversification, the potential benefits of incorporating leverage judiciously, and the value of considering how different assets might perform in various economic scenarios are all insights that can inform personal investment strategies.

Case Study: The Paradox of Low-Volatility Investing

Pim van Vliet has been at the forefront of challenging conventional wisdom about the relationship between risk and return in the stock market. He is the Head of Conservative Equities and Chief Quant Strategist at Robeco, and author of the book High Returns from Low Risk.

Most cases, you take risk, you don't get the reward, and that's an important lesson also for starting investors who think that risk is like Karma: you take risk and then you get the return. That's not the case. ~ Pim van Vliet

Van Vliet's work focuses on the "low-volatility anomaly," which contradicts the traditional Capital Asset Pricing Model (CAPM) theory. According to CAPM, higher risk should lead to higher returns. However, van Vliet's research has consistently shown that low-risk stocks actually generate higher returns, which challenges this fundamental assumption.

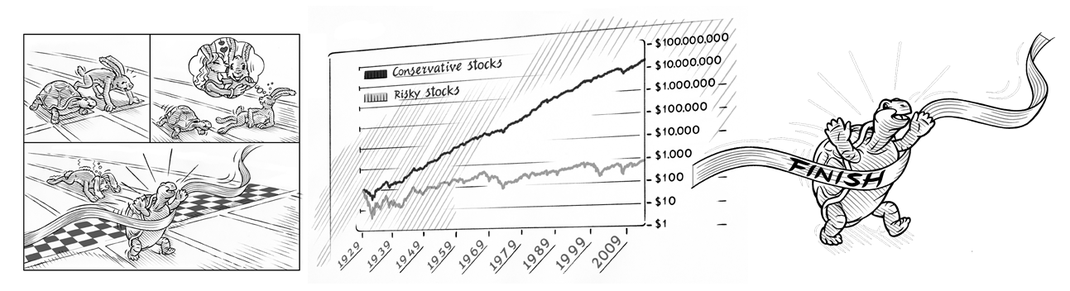

In his studies, van Vliet found that over long periods, low-volatility stocks not only provided better returns but did so with substantially lower risk. For example, in one analysis spanning from 1929 to 2015, a low-volatility portfolio significantly outperformed a high-volatility portfolio. The low-volatility portfolio yielded 10.2% per year, while the high-volatility portfolio provided an annual return of only 6.4%.

Van Vliet's approach to constructing low-volatility portfolios involves several key steps:

- Focusing on the largest stocks by market capitalization to ensure liquidity.

- Measuring historical volatility over a three-year period.

- Ranking stocks based on their volatility.

- Selecting the least volatile stocks for the portfolio.

One of the most intriguing aspects of van Vliet's findings is the explanation for why this anomaly persists. He suggests several reasons:

- Professional investor behavior: Asset managers, whose performance is evaluated against a benchmark, tend to overlook low-risk stocks in favor of potentially higher-performing (but riskier) options.

- Career concerns: The fear of underperforming peers or benchmarks can lead professionals to chase high-risk stocks.

- Business incentives: Asset management firms may be incentivized to sell high-risk funds.

- Psychological factors: Low-risk stocks are often perceived as less exciting and lack the "lottery ticket" appeal of high-risk stocks.

Van Vliet's research also explores how to enhance low-volatility strategies. He suggests combining low volatility with other factors such as income (dividend yield) and momentum. This approach, which he calls the "conservative formula," aims to select stocks that are not only low-risk but also offer attractive income and positive price trends.

The practical application of van Vliet's research has led to the creation of several successful investment products. For instance, he has been involved in managing low-volatility equity funds that have attracted billions in assets under management.

For individual investors, van Vliet's work offers several important lessons:

- Challenge conventional wisdom: High risk doesn't necessarily lead to high returns.

- Consider low-volatility strategies: These can provide attractive risk-adjusted returns over the long term.

- Look beyond volatility: Combining low volatility with other factors like income and momentum can enhance returns.

- Be patient: Low-volatility strategies may underperform during strong bull markets but tend to outperform over full market cycles.

Van Vliet's research also highlights the importance of behavioral finance in investing. By understanding why others might overlook low-risk stocks, investors can potentially capitalize on this market inefficiency.

For individual investors, the work of van Vliet offers several important lessons. First, they challenge the conventional wisdom that high risk necessarily leads to high returns. Second, they highlight the potential benefits of considering low-volatility strategies as part of a long-term investment approach. Third, they suggest that combining low volatility with other factors like income and momentum can potentially enhance returns.

However, it's important to note that low-volatility strategies may underperform during strong bull markets, which is probably why investment advisors stay away from implementing it for all but the most sophisticated investors, one that understand the nature of volatility.

Case Study: Man Group Targets Risk, Not Returns

The Man Group has $170B under management. Their researchers focus on volatility as a key measure of financial risk, and incorporate volatility into their portfolio construction and risk management processes.

- What is volatility? Is risk volatility?

- The Impact of Volatility Targeting

- Volatility is Back: Better to Target Returns or Target Risk?

While their work is perhaps slightly too technical to cover here, here is a summary of the various applications:

- Volatility as a Risk Measure: Volatility is used as a key measure of financial risk. They incorporate volatility into their portfolio construction and risk management processes.

- Volatility Targeting: Man employs volatility targeting strategies, which involve dynamically scaling up the portfolio at times of low volatility, and scaling down at times of high volatility. This approach aims to maintain a more consistent level of risk over time.

- Risk Overlays: Man implements various risk overlays that use volatility as a key input. These include: a) Volatility-switching overlay: This reduces portfolio exposure when volatility spikes. b) Momentum overlay: This reduces exposure to assets in a downward trend. c) Correlation overlay: This adjusts exposure based on the correlation between different assets. d) Diversification-benefit overlay: This reduces portfolio risk when diversification benefits decrease.

- Portfolio Optimization: Man uses volatility forecasts in their portfolio optimization process. They employ techniques like factor models and hierarchical clustering to improve the robustness of their covariance estimates.

- Leverage Management: The firm uses volatility measurements to manage leverage in their portfolios. They may increase leverage for low-volatility assets and decrease it for high-volatility assets to balance risk across different investments.

- Dynamic Risk Management: Man implements dynamic risk management strategies that adjust portfolio exposures based on changing volatility conditions. This includes setting exposure constraints based on both beta and net notional exposure.

- Volatility as an Investment Theme: Man recognizes volatility as a potential source of returns, considering it as part of the "alternative beta" universe. They explore strategies that can benefit from volatility exposure or the volatility risk premium.

In Conclusion

Understanding volatility is a powerful tool for navigating the ups and downs of the stock market. It can help investors assess risk, construct more resilient portfolios, and make more informed decisions about their investments. Market volatility is a normal part of investing. By understanding it and preparing for it, we can avoid making panic-driven decisions and stay focused on your long-term financial goals.

While market losses may be concerning, they also present an opportunity to reassess an investment strategy and ensure it aligns with one's risk tolerance and goals. Whether we decide to adjust our portfolio, increase our cash holdings, or stay the course, decisions should be guided by a clear understanding of volatility and our personal financial situation, rather than by fear or short-term market movements.